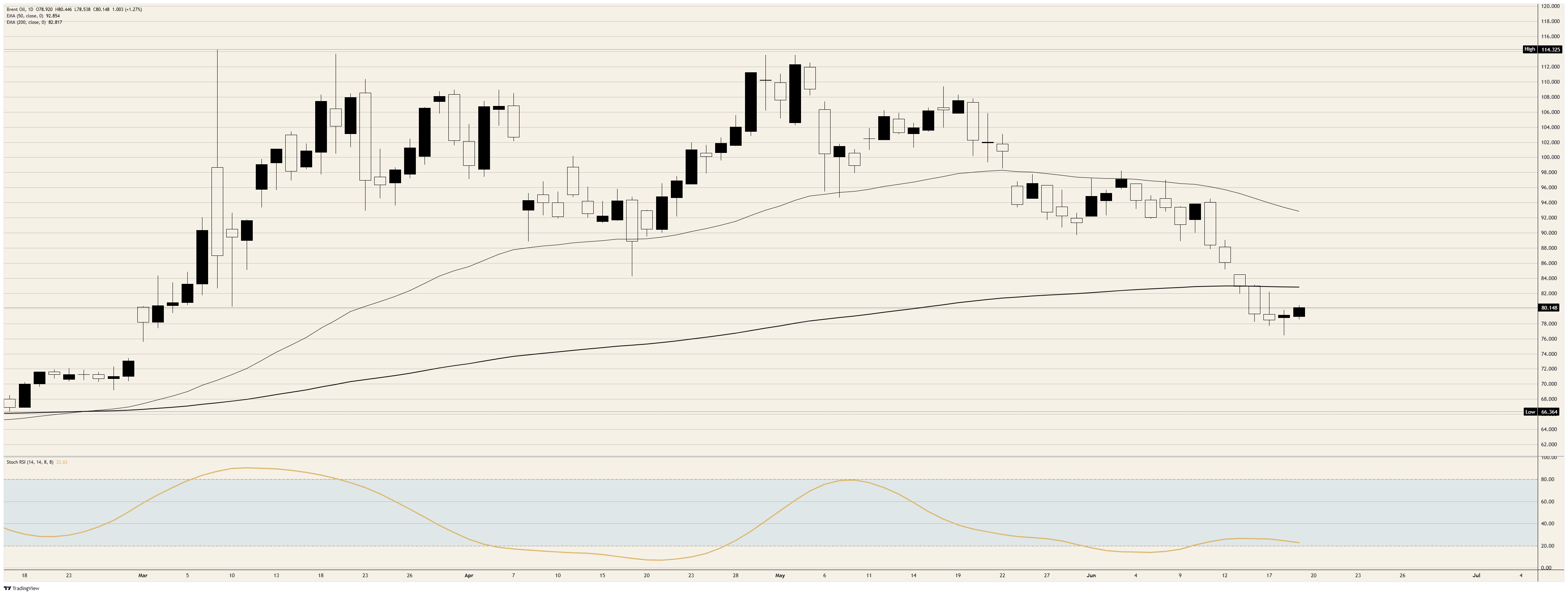

Brent is back near $80 and West Texas Intermediate is back near $77, meaning the oil market has given back almost all of the premium it generated during nearly four months of open war with Iran. On tape, this week’s U.S.-Iran memorandum is treated as a completed peace: the blockade lifted, the Strait of Hormuz reopened, the sale of Iranian barrels allowed, stock prices at record highs, and the president dealing triumphantly with falling pump prices.

The problem is that the market did the exact same transaction in April, priced everything in one session and was cornered within hours, while the people who could actually break the ceasefire were never asked to sign it. There’s nothing about the way this deal is structured that says the second try will end any differently.

The completely lucid option was priced first

Since fighting began on February 28, Brent and WTI oil prices have risen more than 45%, with obsolete Brent cargoes printing above $120 at peaks as traffic at Hormuz ground to a halt and cargoes in the Persian Gulf declined. This bonus no longer exists. In just one week, Brent has lost about 8% and is now around $80, and crude oil has wiped out almost all war gains and is trading close to the level on the day the first rockets were launched.

Risky assets made the same decision – US stocks hit record highs and the president yelled on Truth Social about falling oil prices and cassette tapes while labeling his critics as jealous or stupid. Read carefully, the market is right: the deal exists, it has been signed and the ships are sailing. Read what the contract actually entails, reducing risk seems early.

Opened on paper, extracted in water

Start with what all the traffic is pricing in: the reopened Strait of Hormuz, the artery through which roughly one-fifth of the world’s oil flows. It is open, but only at the edges. Tanker industry trackers kept the main central channel still closed, with approximately 80 mines remaining to clear; traffic is routed through the northern route in Iranian waters and the southern route covering the coast of Oman, with US Central Command (CENTCOM) lifting port restrictions and naval advisories directing ships towards Oman to avoid mines.

Even the flow of goods is measured by Iran’s Islamic Revolutionary Guard Corps (IRGC), which openly limits the number of ships to manage congestion. Tehran is already fighting over terms: where Washington has pledged free opening, Iran says no such clause exists and that it will operate the waterway based on its own arrangements, inspections, services and security. Iran is therefore providing market-provided supply relief, at Iran’s pace, reversible on its word. This is not a standardized strait. It’s a faucet with Tehran’s hand on it.

Bilateral Agreement on Tripartite War

Here’s the part the price action ignores. The Memorandum of Understanding (MoU) is a 14-point bilateral document signed by President Trump in Versailles and Iranian President Masoud Pezeshkian in Tehran. The war he seeks to end is not two-sided. Its most perilous front runs through Lebanon, where Israel is fighting Hezbollah and Israel has never signed anything. The text calls for an end to the war on all fronts, including Lebanon; Israel’s defense minister said directly that Israeli forces would hold the occupied areas in Lebanon, Gaza and Syria for an indefinite period of time.

The gap is not academic because Iran has already found leverage in it. Technical talks scheduled to begin today in Switzerland ended before they began, with Iran halting its delegation on Israel’s campaign in Lebanon and demanding that Israel withdraw first. So the 60-day clock to push Iran toward the nuclear deal is a clock Iran can stop whenever Israel pulls a trigger over which Iran has no control. Three unrelated actors, Israel, Hezbollah and Iran’s hardliners, could break it, and the president’s assurance that he could keep Israel in check came hours before Israel began the second deadliest day of the war in Lebanon, with the government in Beirut counting 47 dead.

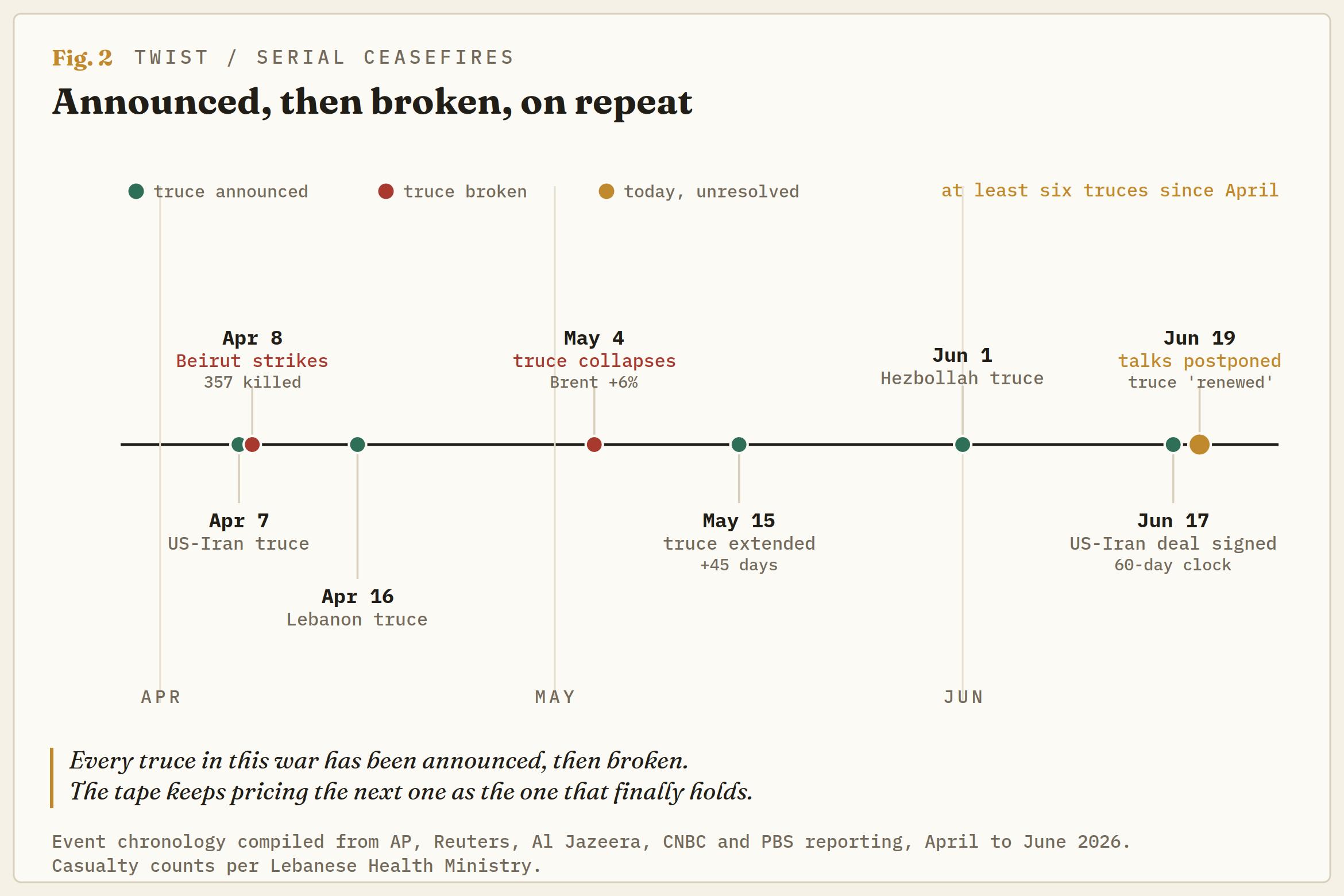

April has already done this experiment

The reason for distrust of a round-trip solution is that the market has experienced it. In early April, Washington announced a two-week ceasefire, and the price of oil fell by approximately 16% in one session, with the price of Brent crude falling to low levels of $90, following the same logic that drives today’s tape. Within hours, Israel struck Beirut in what it considered the heaviest attack of the war, killing over 350 people, and the truce was broken.

At the beginning of May, there was a complete breakout: Brent jumped 6% in one day, again above $110, WTI strengthened at $100, Dow lost over 500 points, and the volatility of the offer returned. The market then weakened the war premium and produced a reversal. It is now changing it again, from a lower basis, to an agreement whose first procedural step has already failed. The number of serial truces is clear. The ceasefire in Lebanon itself has been concluded, broken and renewed at least five times since April, and today’s version was released only after one of the bloodiest days of the conflict and there is still no confirmation from the Israeli army or Hezbollah. A ceasefire that needs to be declared again is often not peace. It’s a break for better public relations.

Where the skinny guy sits

The tape priced a 60-day transition to a constant contract. The problem is that the premium is too inexpensive for a window where three spoilers can blow up. Brent at $80 is a level that the market is defending, and the drivers of the augment write themselves: any incident in Hormuz, any challenging break of the ceasefire in Lebanon or Iran going off the nuclear track over time. Each of them drives the tape back towards $90, and a true closure of the strait reopens the above-$100 regime that the market has been working towards for weeks.

The other side is also forthright: If the side routes remain open, the mines come out, and next week’s meetings in Washington hold Lebanon together, the premium will continue to fall toward the low base of $70 that prevailed before the war. However, the risk/reward ratio leans towards keeping some war option current rather than selling the last one near $80. The contract has been signed. The people who never signed it will decide whether it will be valid.

Brent Spot, daily chart

{kind=link}