Image source: Getty Images

TescoThe company’s (LSE:TSCO) share price has been withering since today’s first-quarter trading announcement. It fell another 2% after the statement was released, suggesting investors weren’t expecting much and yet came away disappointed.

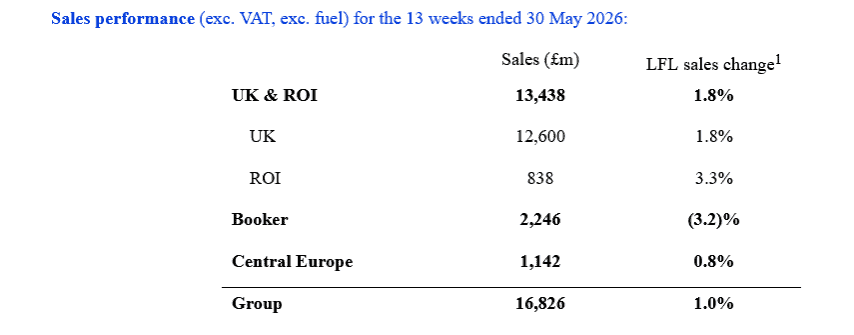

What happened? Tesco’s comparable revenues in the three months to May were up just 1% year-on-year, excluding fuel. City analysts expected their growth by 1.4%.

The thing is, I think the situation could be much more arduous FTSE100 company and its share price. Want to know why?

Disappointing Q1

Food retail is one of the most stable industries in the world. Tesco is the biggest player in the industry, with millions of true customers and incredible scale that helps keep costs low. Analysts in RBC Capital described the company as

A best-in-class UK food retail player, with a forceful business model and experienced management team.

It is quite possible that you shop at Tesco yourself in a stationary or online store. I dropped by a local place this morning to pick up some of the basics. But for all its advantages, Britain’s largest retailer remains at the mercy of the country’s ongoing cost of living crisis. And it’s now feeling a bigger impact than analysts predicted.

As the above numbers show, Booker’s wholesale division achieved the worst performance in the first quarter. This reflected arduous year-on-year comparative data and the termination of a lower margin contract.

However, the main problem is concerns about Tesco’s trading activities in the UK. It is the engine room of the company’s operations, generating approximately three-quarters of revenues. Comparable sales rose 1.8% in the first quarter, exactly half a percentage point below analyst expectations.

There is no room for mistakes

The problem with Tesco shares is that, historically, they tend to be exorbitant. At 448p per share they are trading forward price-to-earnings ratio (P/E). about 15 times. This is higher than the 10-year average of 11-12 years.

It’s definitely not outrageously exorbitant. However, any overpriced stock must at least consistently beat broker forecasts. This certainly hasn’t happened for Tesco today, hence the decline in its share price.

The problem is that sales may remain under pressure in the coming months, which could lead to more disappointing trading statements. If this happens, you can expect a forceful recommendation for Tesco shares.

What could go wrong?

One danger is that consumers will continue to feel inflationary pressures. Also in this situation, Tesco will have restricted ability to pass on rising costs to customers, which will affect margins.

Finally, the revival of competitors in the famously competitive food retail segment may have an impact on Tesco’s sales. As analysts from RBC Capital also mention,

Market share growth has been moderate in recent periods and we expect this trend to continue as UK competitors begin to stabilize their volume losses.

I certainly won’t take any risks with Tesco shares today. Especially considering the company’s high market valuation on the FTSE.

Is it worth investing £5,000 in Tesco Plc now?

If investing expert Mark Rogers and his team have stock advice, it can pay to listen. After all, Twelfth Magpie’s flagship Share Advisor newsletter, which it has run for almost a decade, provides thousands of paying members with the best share recommendations from across the UK and US markets.

Mark believes there are 6 standout stocks that investors should consider buying right now. Want to check if Tesco Plc is on the list?

Royston Wild holds no position in the companies mentioned.

{kind=link}