With Bitcoin falling below $60,000 and Strategy’s stock price down more than 70% from its high, some cryptocurrency investors are wondering whether Strategy could become this cycle’s Terra/LUNA – a highly leveraged bet on a cryptocurrency market structure that will explode under stress.

The company’s response? The recent capital framework published on Monday was intended to allay investor concerns.

The package includes a repurchase of up to $1 billion of MSTR, a repurchase of up to $1 billion of STRC and related securities, an boost in STRC’s dividend to approximately 12%, and an boost in the cash buffer to $2.55 billion.

Of particular note for a company known for its maximalist approach to Bitcoin, Strategy also said it may sell up to $1.25 billion worth of BTC holdings if necessary to meet dividend or debt obligations.

Markets he replied welcomed the news, with shares of STRC and MSTR rising more than 12% in after-hours trading. STRC is currently trading at $84.86, a significant improvement from the $72.06 it traded on June 26.

STRC’s share price rose more than 12% in after-hours trading. Source: : Yahoo Finance.

But will the plan be enough to allay concerns that the STRC structure – famously dreamed up by CEO Michael Saylor with the lend a hand of the LLM – could expose Strategy to a “death spiral” of reflective financing risk during periods of market stress?

What is STRC and why is it controversial?

STRC is part of Strategy’s capital structure tied to the broader Bitcoin Treasury Strategy. This sits between time-honored equity and debt-like instruments, offering investors a yield while maintaining exposure to the company’s Bitcoin holdings.

Related: MSTR Strategy could fall 80% if it repeats this dot-com era fractal

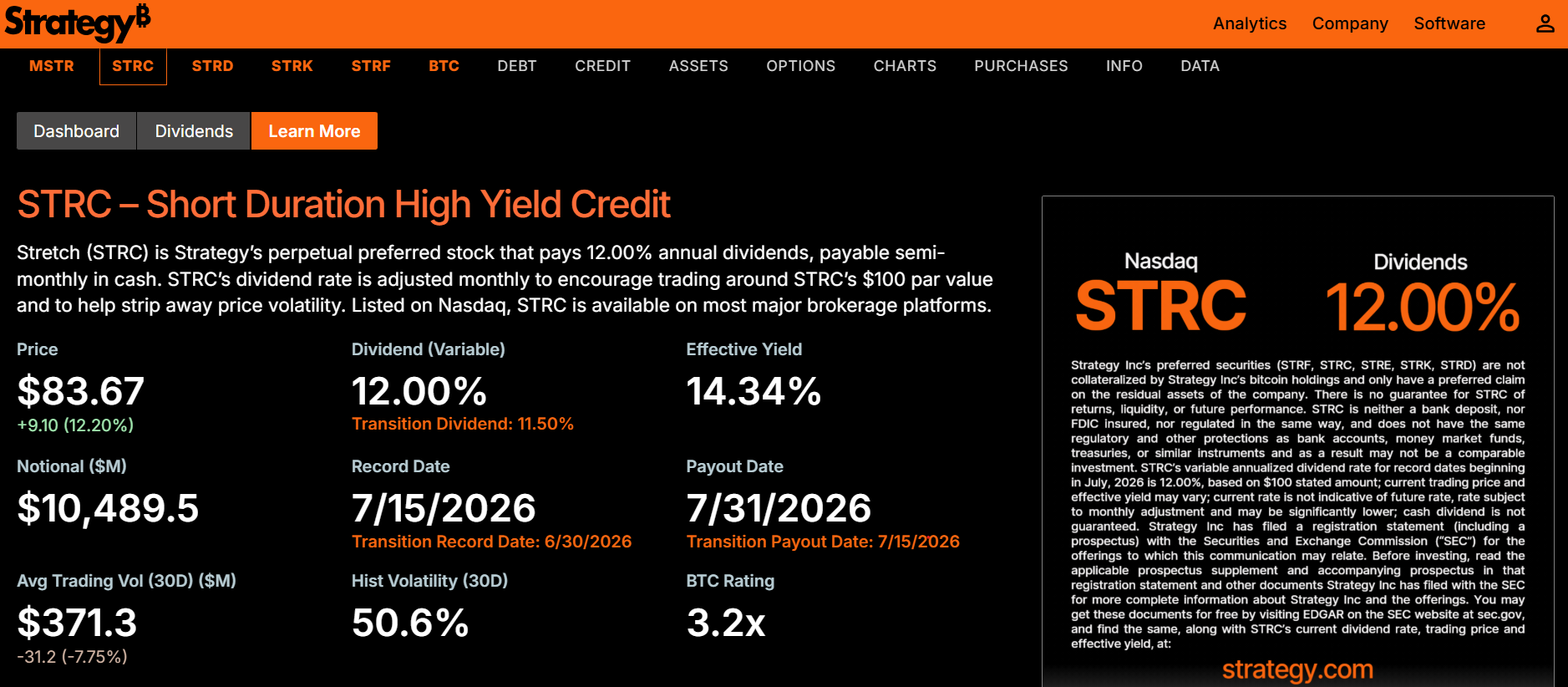

The strategy describes STRC as a perpetual preferred stock paying a 12% annual dividend with a par value of $100, funded by cash reserves and a Bitcoin-pegged capital framework.

While the structure is designed to provide financing flexibility without issuing time-honored debt, analysts have wondered whether its stability depends on continued investor demand in secondary markets, particularly during periods of Bitcoin volatility or tighter liquidity conditions.

Strategy’s common shares are called MSTR and represent shares in Strategy’s capital along with voting rights. The fates of the two securities are closely related, but different. Likewise, Strategy’s position as Bitcoin’s largest buyer (and perhaps future seller) means its fate is closely tied to Bitcoin’s current price.

Perennial goldbug and Bitcoin critic Peter Schiff has repeatedly called for the strategy model: pointing that he “cannot sell Bitcoin without the Bitcoin price collapsing. Even if Strategy simply stopped buying Bitcoin, that change alone would crush the market.”

The strategy describes STRC as a short-term, high-yield loan. Source: Strategy

However, Taran Dhillon, director of digital assets at Kula, told Cointelegraph that “Bitcoin’s volatility alone is unlikely to break a structure like the strategy.”

He said a more significant test is “whether Bitcoin will remain under pressure as access to capital becomes more expensive or difficult.”

Bear case: feedback loops and liquidity dependence

Some argue that Strategy’s entire fundraising and equity model is inherently reflexive, combining both boom and bust cycles. The same flywheel that amplify profits in bull markets can accelerate losses in bear markets, when falling Bitcoin and stock prices collide with weaker demand.

This is exactly what Ripple CEO Brad Garlinghouse expressed point this week on CNBC. “Financial engineering does not create long-term value,” he said.

Kyle Rodda, senior analyst at Capital.com, told Cointelegraph that Strategy effectively operates as a momentum-driven Bitcoin accumulation vehicle where capital raises funds to purchase Bitcoin, which in turn supports the company’s valuation. However, he warned that under stress the dynamics could reverse.

“The Strategy business is clearly adding momentum in both directions,” Rodda said, adding that in weaker conditions, rising financing costs and degenerating investor appetite could reinforce downward pressure.

Related: Grayscale’s Pandl says Strategy should sell $3 billion worth of Bitcoin to restore confidence

He also argued that secondary market liquidity is a structural relationship, meaning that pressure to sell or refinance on a vast scale could have wider spillover effects on the Bitcoin markets themselves.

Among Bitcoiners, Charles Edwards, founder of Capriole Investments, has been one of Strategy’s most hawkish commentators in recent times.

He compared the stress in digital asset treasure companies to broader cryptocurrency deleveraging events, warning that feedback loops could accelerate losses as leverage and sentiment deteriorate.

“Is anyone else feeling the LUNA 2022 vibes at MicroStrategy?” He sent June 26.

Strategy comparison with Terra/LUNA. Source: Charles Edwards

Neutral View: The real risk is funding the markets, not Bitcoin

As bearish sentiment around the Strategy grows on X, Dhillon told Cointelegraph that stresses will likely first emerge in financing conditions, pointing to rising discounts, higher yields and reduced issuance capacity as early warning signs.

In his view, Strategy’s holdings of Bitcoin are less significant than whether the company can continue to refinance or rollover capital efficiently during periods of market stress.

And while STRC’s failure to maintain its “peg” at $100 has caused much consternation, STRC is not pegged to $100 in the same way that a stablecoin is pegged to $1. The yield simply becomes more attractive the further the price drops below $100, which should theoretically cause buyers to drop the price to $100 at some point.

A Bitfire Research report shared with Cointelegraph concluded that STRC’s recent price fluctuations should not be interpreted as a structural failure.

The company argued that unwinding events are largely driven by sentiment and liquidity conditions, rather than changes in the Strategy’s underlying fundamentals or solvency profile.

“Strategy (formerly MicroStrategy) is not at risk of insolvency in the near future,” the company wrote.

The bull case: stress does not mean insolvency

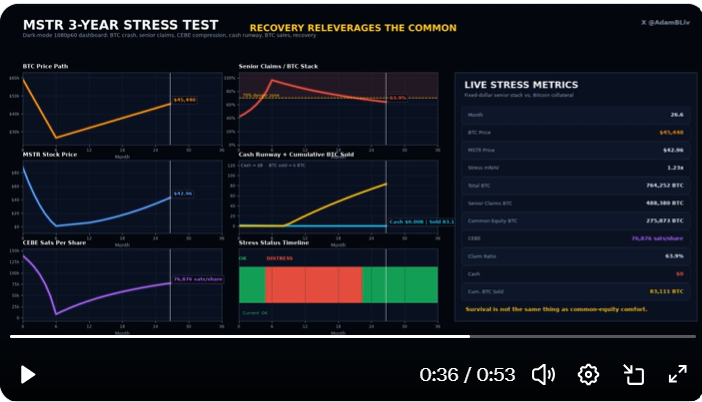

Strategy supporter Adam Livingston, supporter and author of Bitcoin, he ran what he described as a “three-year stress test of MSTR” under extreme conditions, including a 55% Bitcoin payout, closed capital markets, and a constant cash burn requiring vast Bitcoin sales to meet obligations.

Related: CryptoQuant Warns on Strategy’s Dividend Coverage Due to 38% Drop in Cash Reserves

In his model, Strategy’s preferred claims boost dramatically in Bitcoin terms, while the company’s “Bitcoin common stock exposure” (CEBE) decreases significantly. He described it as the “annihilation of CEBE” and dropped from 138,161 sat per share to 7,884 sat per share at the lowest point of the simulation.

Death spiral? This model says no. Source: Adam Livingston

The model assumes no recent Bitcoin purchases or equity issuances during the downturn, with approximately 115,727 BTC sold over three years to service liabilities before stabilization conditions return.

Despite the severity of the decline, Livingston’s model ultimately shows that the strategy will survive the cycle, ending up with over 700,000 BTC remaining on its balance sheet and a recovering net asset structure once market conditions normalize.

What strategy actually changed

The recent framework represents the Strategy’s clearest attempt yet to address concerns around liquidity and reflexivity risks.

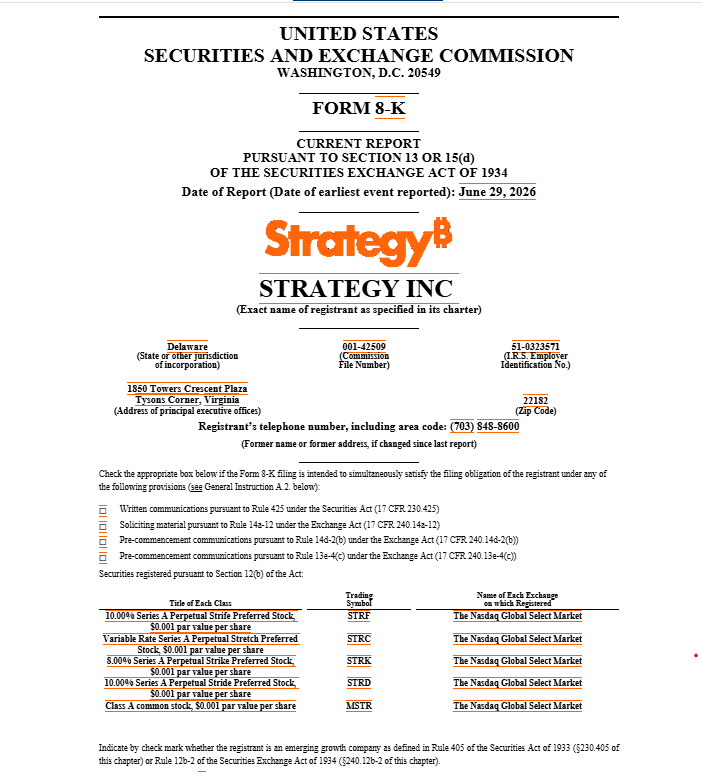

Key elements of the June 29 8-K strategy filing which are aimed at restoring confidence in the company, include the buyback of MSTR and STRC shares and a mighty emphasis on increasing cash reserves for dividend payments. The nuclear option to sell up to $1.25 billion worth of Bitcoin holdings for dividend payments was included in part to keep markets unthreatening Bitcoin maximalist Michael Saylor is reluctant to sell the asset if forced to do so.

Related: Bitcoin Price Has Fallen Over 40% Since STRC Launched: Is the Strategy “OK”?

8-K Strategy filing, June 29. Source: U.S. Securities and Exchange Commission

Dhillon said the framework “significantly improves” the transparency of the Strategy’s response to challenging conditions, with an increased $2.55 billion reserve and a clearer Bitcoin monetization plan helping to strengthen investor confidence.

But Schiff he noticed that MSTR’s current market capitalization is $30 billion, while its Bitcoin’s current value is $50 billion. “Unless MSTR’s market capitalization increases above Bitcoin’s value, each Bitcoin purchased through the MSTR share issue generates a negative Bitcoin yield,” he said.

Stronger toolkit, same basic plant

While the framework strengthens the Strategy’s ability to deal with short-term stresses, it does not eliminate its dependence on capital markets to maintain its broader Bitcoin accumulation strategy.

As Dhillon told Cointelegraph, the key test will be whether financing conditions remain available during periods of market stress, rather than Bitcoin’s price action itself.

He added that the update clarifies the Strategy’s capital allocation scheme and provides management with a more defined sequence of actions, making the overall strategy more credible.

For critics like Rodda, the basic concern remains unchanged. The structure of the strategy remains vulnerable to feedback loops in the event of liquidity constraints in both the equity and credit markets.

While Strategy’s move introduces clearer liquidity buffers, redemptions and contingency options, including a potential Bitcoin sale, the debate on structural reflexivity has not yet been fully resolved.

The question now is not whether STRC is inherently frail in theory, but whether Strategy’s expanded toolkit can withstand a prolonged period of capital market stress and whether investors still want exposure to a tool that amplifies Bitcoin cycles and increases risk, rather than simply tracking them.

Warehouse: Bitcoin won’t reach $1 million by 2030, says veteran trader Peter Brandt

{kind=link}