Whatever you think Tesla (NASDAQ: TSLA), this is a supply that seems to be missing.

The very look at the chart of share prices already indicates wild fluctuations in the moods that we saw about Tesla on the stock exchange at various points.

36%has dropped since the beginning of the year. This is a great fall for every company, not to mention what – even after autumn – requires market capitalization of over USD 800 billion.

Despite this, the share has increased by over 50% over the past year. Within five years, things look even better: shareholders in this period are now sitting on 437% augment.

Tesla seems to be confused by many investors

So what’s going on here?

Some movements reflect almost meme features of Tesla for a company of their size, with many investors have a sturdy view based on factors such as their opinion of the Chief Director.

But most meme shares have at most market capitalization of several billion dollars. I think something completely different is happening when it comes to Tesla’s actions: even many sophisticated investors are really confused as to appreciate.

Is it a car manufacturer with attractive profit margins in recent years, now seeing the level of sales?

In this case, even by adding additional value for rapidly developing activity in the field of energy production, the current market capitalization looks like me. Is 20 times greater than market capitalization FerryFor example.

Or, is Tesla really an investment case regarding the proven ability to innovate and disruption of mass industries, as it has already done with cars and can do it with taxis and robotics? In this case, I see the argument that Tesla is potentially a long -term opportunity at the current price.

Investing in facts, not hope

Tesla did a very impressive work when it comes to business development. Revenues have increased in recent years. Division into a quarterly revenue number, and as the chart below shows, there is now a clear reason for Tesla investors.

Created with TradingView

This week, the company announced a pathetic first quarter when the company is fighting fires on many fronts. Not only did he see the falling sales, but also the profits fell. In the first quarter, revenues fell by one fifth compared to the same period last year.

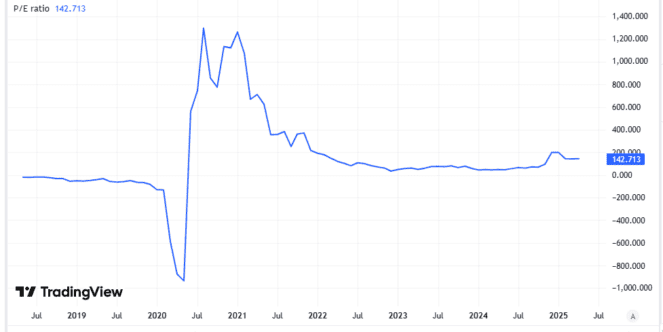

Meanwhile, profit per share (on the basis of generally accepted accounting rules) fell by 71% compared to the same quarter of last year. Already, the price ratio to Tesla’s profit (P/E) of 143 looks too high to consider investing. But if the earnings fall, the valuation will look even less attractive.

Created with TradingView

I see hope for a non -automotic business. In the first quarter in the first quarter in the first quarter, energy production increased by 67% of the year. But still constitutes only about 15% of total revenues.

For now, at least energy and pipeline production projects, such as automatic taxis, look too unverified to justify the current quote of Tesla. Along with growing competition, vehicles also look exaggerated to me.

To sum up, based on current facts, not future hopes, I see Tesla’s actions as overstated and will not invest.

{kind=link}