Image source: Getty Images

Parents can pay as little as £2,880 a year into a child’s SIPP (Self-Invested Personal Pension) – with the Government increasing this to £3,600. Given enough time, the results are remarkable.

The mechanics are uncomplicated but powerful. Parents and grandparents can contribute up to £2,880 a year to their child’s SIPP – and even though the child pays no tax, the government adds a 20% allowance, bringing the total annual contribution to £3,600. That’s all. Here’s the whole strategy.

Let’s assume that the parents, and then the child, maintain this contribution for another 55 years. It must be admitted that at the end of this period – in about 50 years – the premiums will actually be quite compact in relation to the value of money.

Time does the challenging work

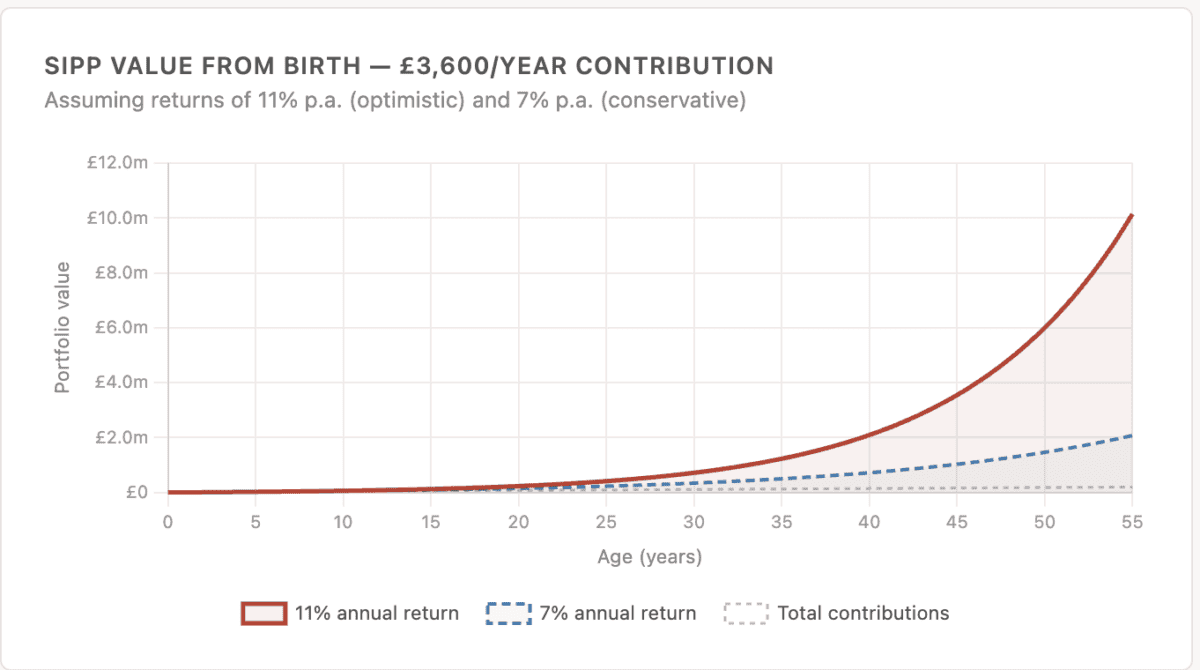

Assuming the money is invested in global stocks that return 11% per year – essentially in line with the norm S&P500the company’s performance over the last 55 years – this modest contribution adds up to something extraordinary. After 20 years, the pot is around £230,000. After 35 years, £1.2 million. By the age of 55, just over £10 million.

What’s really striking is how much of this growth happens at the end. The last decade alone has added over £6 million – more than the previous 45 years combined. Here’s what mixing actually means in practice: the longer it lasts, the faster it accelerates. The total amount paid out over 55 years is just £198,000. The rest – over £9.9 million – is pure growth.

There are, of course, caveats. According to the regulations that will come into force in 2028, the money will be kept until at least the age of 57. A return of 11% is not guaranteed – markets can disappoint for years.

Many families simply cannot budget £2,880 a year from birth. But it’s worth playing with the numbers. Even compact donations – say £20 a month – can make a huge difference over time.

Where to invest?

For long-term SIPP investors, few investment funds make a stronger case than A Scottish mortgage investment fund (LSE:SMT).

An investment fund run by Baillie Gifford does something most retail investors can’t: gain access to unique private companies before they go public.

This is clearly noticeable in its larger holding company – SpaceX. The company is valued at £800 billion on Scottish Mortgage’s balance sheet, but that could double if SpaceX goes public this year – it already accounts for around 16% of the portfolio.

The company also provides investors with instant diversification with many household names and companies you’ve never heard of.

The philosophy is patience – positions are held for years, sometimes decades, ignoring short-term noise. This comes with real risks: confidence has fallen by more than 50% in 2022 amid a edged revaluation of growth stocks. Moreover, concentrated private holdings can be illiquid and tough to value accurately.

However, it is certainly an intriguing proposition and worth considering.

{kind=link}