S&P slams the flap

For months, Wall Street has treated the possible inclusion of SpaceX in the S&P 500 index as a foregone conclusion. The premise was basic. Launch the largest IPO in history, wait six months, then pull back as an estimated $14 billion wave of passive money flows into the stock.

On Thursday, S&P Dow Jones quietly pulled the emergency brake.

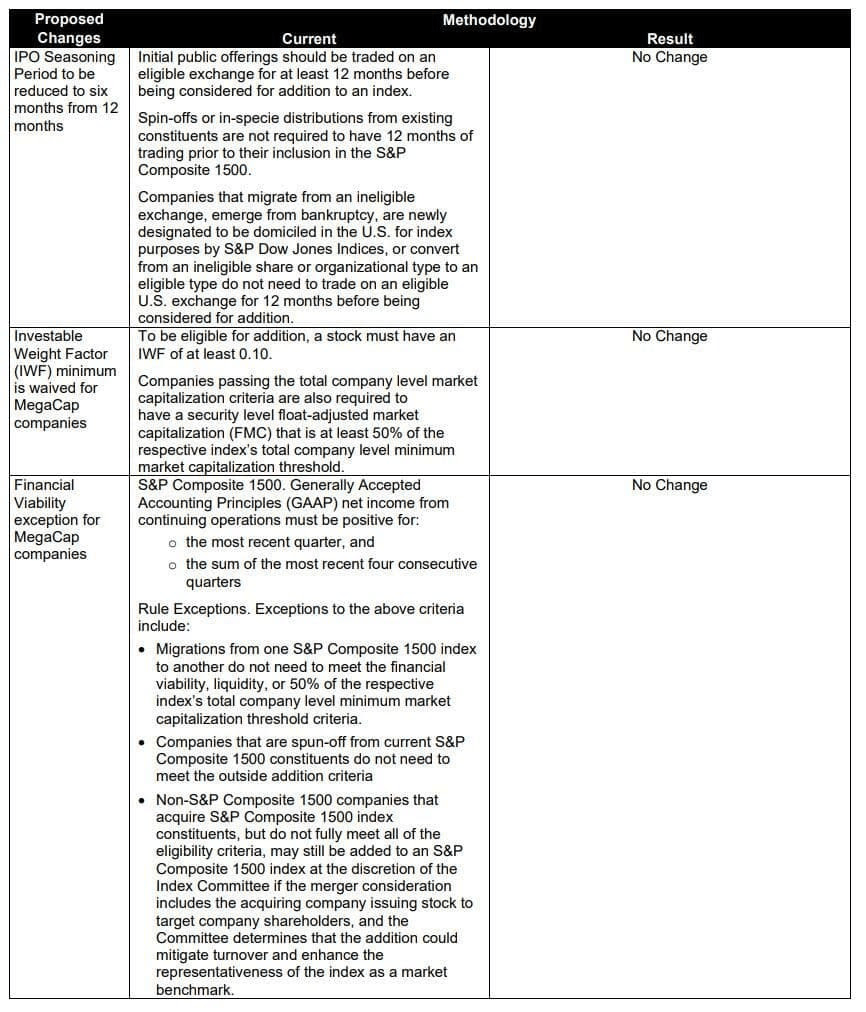

In a move that surprised much of the market, S&P rejected proposals that would have accelerated the listing of large-cap companies. The index owner decided not to shorten the 12-month seasoning period, not to waive the profitability requirements and not to relax the stock exchange trading rules, regardless of the company’s size.

In other words, even a $1.8 trillion rocket won’t cross the line.

The decision effectively leaves SpaceX in orbit outside the S&P 500 lock until at least June 2027. It delays what many investors assumed would be one of the biggest passive allocation events in market history and removes a key pillar of the near-term bullish story around IPOs.

The moment is noteworthy because much of the excitement surrounding SpaceX has never been just about earnings, rockets or Mars. It was about market mechanics. Investors have already been calculating how many billions of dollars index funds will have to spend once their stocks are included in the benchmark. This passive demand has become part of the valuation narrative itself.

S&P’s decision is a reminder that benchmark providers still see their role as gatekeepers, not cheerleaders. The rules were intended to stop indexes from chasing market emotion before a newly listed company had achieved sufficient trading history and demonstrated sustained profitability.

For the broader market, this ruling could actually remove the source of future liquidity problems. If SpaceX were included in the index after just six months, passive funds would need to raise huge amounts of cash by selling existing assets. This would create winners and losers across the market, regardless of fundamentals.

Instead, the liquidity tsunami was simply postponed.

The irony is that Nasdaq and FTSE Russell have already moved in the opposite direction, adopting faster inclusion schedules that reflect the reality that many of today’s tech giants are reaching trillion-dollar valuations well before the opening bell. SpaceX could still join the Nasdaq 100 index much more quickly, unlocking a significant but smaller pool of passive inflows.

For now, however, Wall Street’s most anticipated passenger is stuck in the index eligibility screening stage.

The rocket took off.

Passive fuel tanks will have to wait.

More detailed description of the announcement:

{kind=link}