Key takeaways:

- The strategy struggles with lower short-term liquidity, but conservative net leverage of 11% protects it from forced BTC liquidation.

- Bitcoin’s rise above $70,000 remains unlikely as long as STRC sees trades below $100 and spot ETFs show net selling pressure.

Bitcoin (BTC) faced a 21% price correction in 10 days, retesting the $61,000 level for the first time in 4 months. The move coincided with Strategy’s (MSTR US) decision to buy back some corporate debt, temporarily halting Bitcoin accumulation. Traders now fear that Strategy may be forced to liquidate some of its Bitcoin holdings.

Strategy (MSTR US) Bitcoin Reserve Changes and Average Price. Source: Strategy

The strategy has been the largest known buyer of Bitcoin, accumulating 126,016 BTC for $9.31 billion since March. However, the company benefited $1.38 billion in cash funds obtained as a result of recent share issues to redeem part of the convertible debt. The decision announced on May 15 coincided with Stretch’s (STRC US) preferred stock distancing itself from $100.

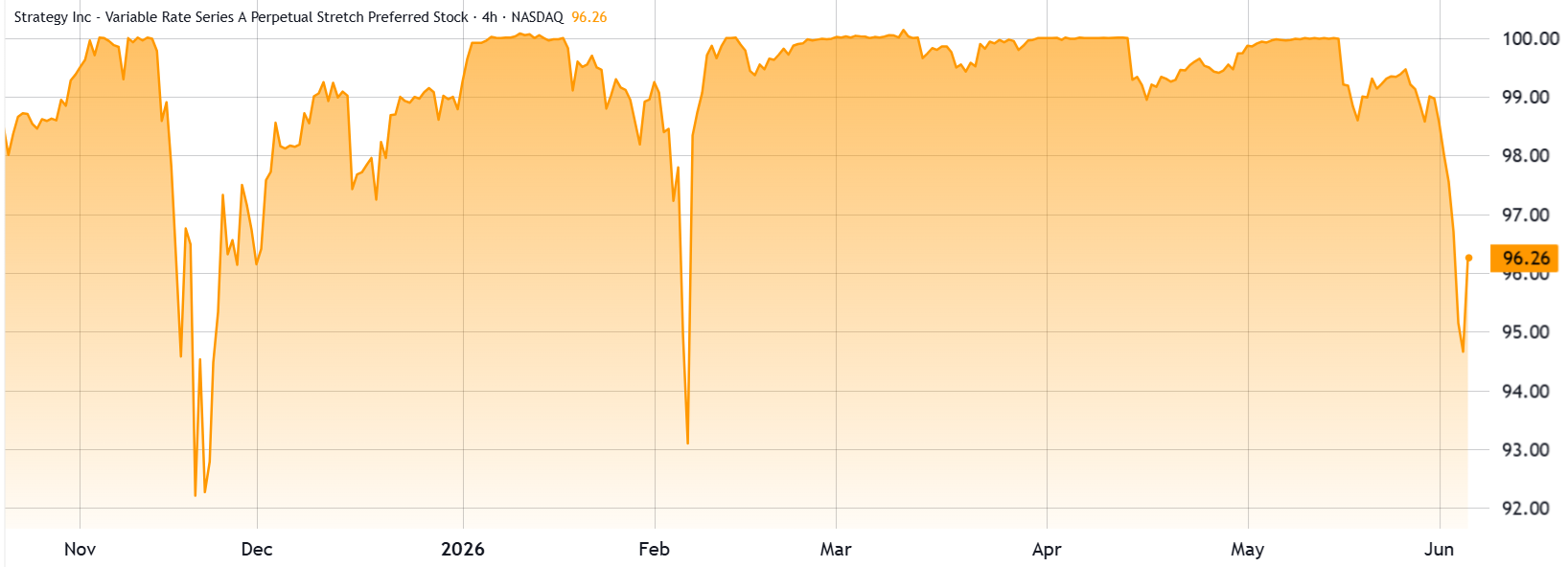

Strategy Series A Perpetual Stretch Preferred Stock (STRC US). Source: TradingView

STRC Preferred Stock allows Strategy to issue recent shares when their price reaches $100 and offers holders a variable dividend, currently set to 11.5% annually, payable monthly in cash. If investors feel it is no longer worth $100, recent buyers step in at lower levels, which is equivalent to demanding a higher dividend. So, at first glance, this should not be a material event for Strategy’s risk perception.

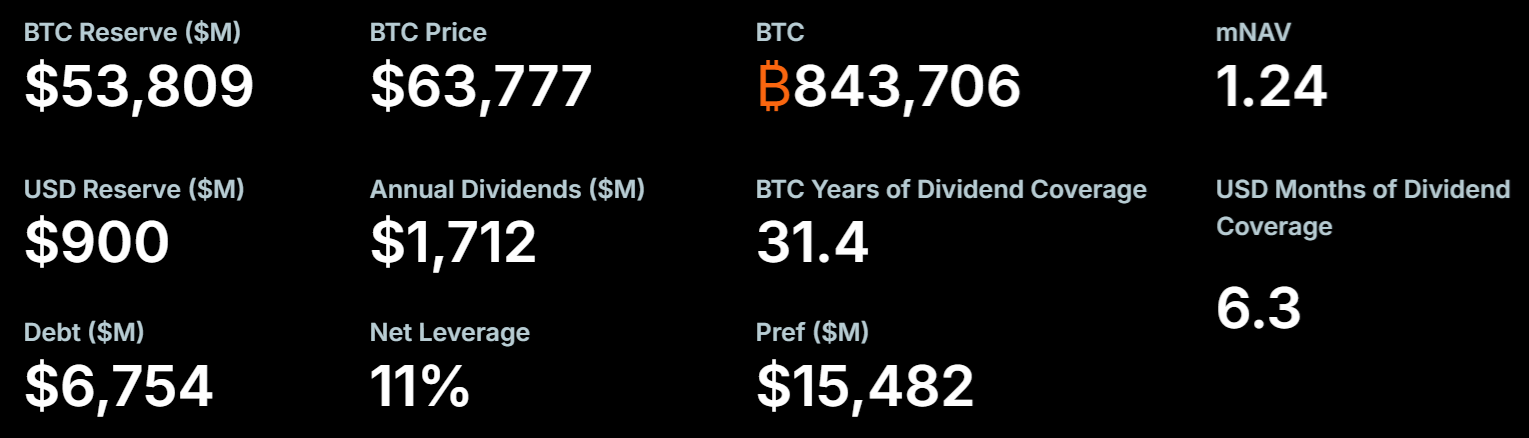

The strategy raised $7.5 billion through preferred stock issuances in the first 5 months of 2026, which largely supported Bitcoin’s price. Currently, the company faces a hard road ahead, considering that its cash position has been reduced to $900 million, which is enough to cover dividends for 6 months.

Strategy Financial Highlights (MSTR US). Source: Strategy

The key financial metric to monitor is the strategy’s 11% net leverage, as it reflects the amount of debt a company holds relative to its assets. By any standard, the range provided by Bitcoin holdings – even at a price of $30,000 – should be considered conservative.

Will Strategy be forced to liquidate some of its Bitcoin holdings?

While short-term liquidity conditions have certainly deteriorated, there is no contractual minimum level of Strategy’s convertible debt that would force the liquidation of Bitcoin reserves. Moreover, there is no prohibition on selling MSTR shares at a discount to the market-adjusted net asset value.

If debt markets are not available, the company may elect to dilute current MSTR holders. Whether this move is interpreted as weakening and further pressure on MSTR and STRC prices is irrelevant to the Strategy’s leverage ratio as the company will remain financially sound.

Related: Saylor downplays Bitcoin’s slide as Strategy faces $11 billion paper loss

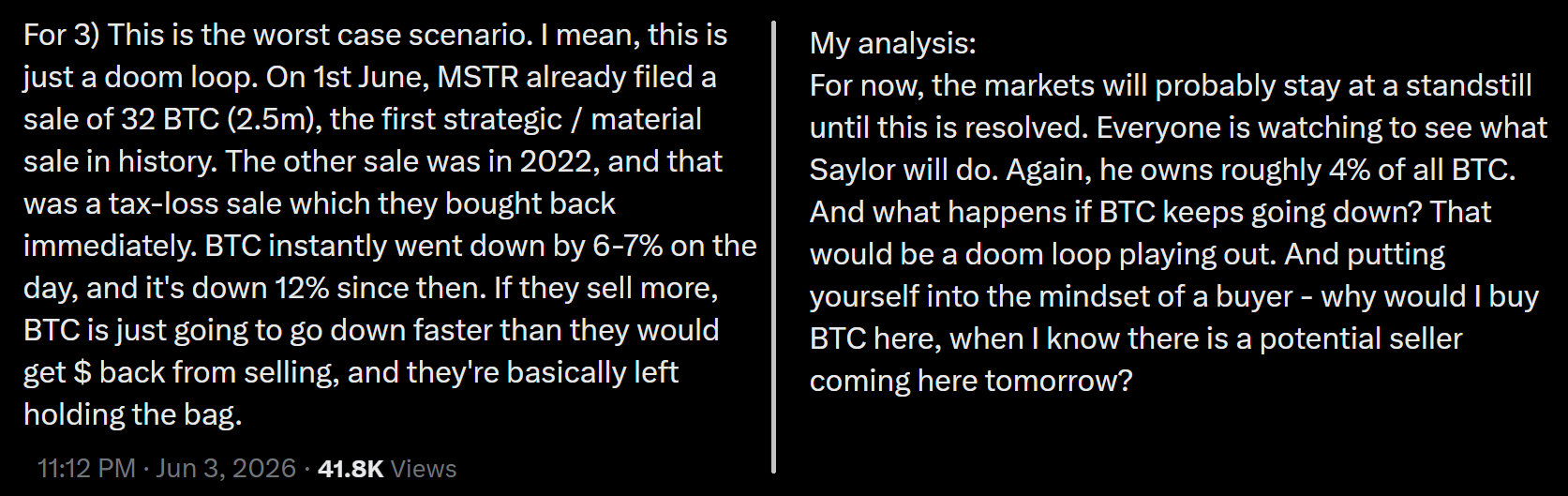

Source: X/zeroxkyle

According to user X zeroxkyle, author of the “Grand Line” newsletter, Strategy’s eventual sale of Bitcoin would only lower its price faster, worsening liquidity conditions. The analysis refers to a “doom loop” in which buyers refrain from adding items due to the constant fear of a enormous seller entering the market.

It is impossible to predict what will ease the tension among investors, as Strategy is not at risk of an imminent forced sale. Preferred stock dividends can be withheld at will, although they only accumulate for later exploit. Still, as long as STRC continues to trade below $100 and spot ETFs remain a net seller, the chances of Bitcoin rising above $70,000 are slim.

{kind=link}