Key takeaways:

- While Bitcoin onchain activity and derivatives show a lack of investor participation, record inflows of cash ETFs indicate mighty institutional demand.

- The lack of leveraged long positions may actually contribute to further growth as sellers are forced to buy back if Bitcoin gains ground.

Bitcoin (BTC) has gained 7% over the past week, surpassing $81,000 for the first time in over three months. Despite mighty price performance, data suggests that Bitcoin derivatives lack investor optimism, raising questions about the sustainability of the rally.

Bitcoin derivatives do not reflect investors’ joy at $81,000

Macroeconomic indicators and several onchain indicators point to weakening demand.

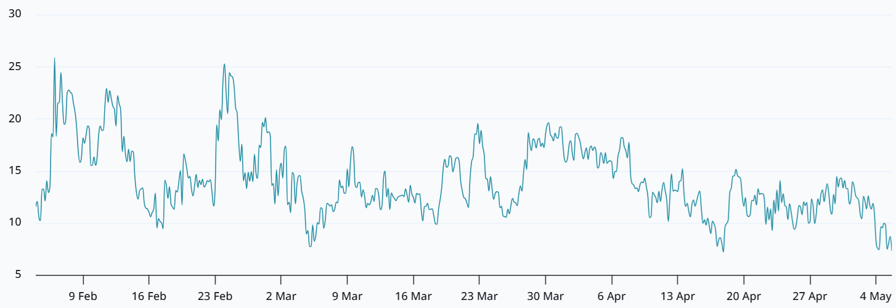

2-month Bitcoin futures base rate. Source: Lightness

On Tuesday, monthly Bitcoin futures were trading at an annual premium of 1% (base rate) compared to spot markets, trading well below the neutral threshold. Typically, sellers demand a premium of 4% to 8% to offset the cost of capital. This cautious attitude continued in slow January, when Bitcoin was trading at $90,000, partly explaining the current lack of enthusiasm.

To confirm whether the issuance is narrow to futures, the demand balance between put (put) and call (call) options must be assessed. In neutral conditions, these instruments are quoted at a premium of -6% to +6% to each other. When professional investors are concerned about the risk of loss, the delta deviation rate increases above 6%.

30 Day Bitcoin Options at Deribit. source: Laevitas

On Tuesday, Bitcoin’s delta deviation approached the neutral 6% threshold, although it remained slightly bearish. The whales and market makers don’t seem particularly concerned about the imminent disaster, but the bulls’ belief has clearly stagnated. With Brent crude oil prices hovering near $110, persistent inflation concerns are weighing on investor expectations for economic growth.

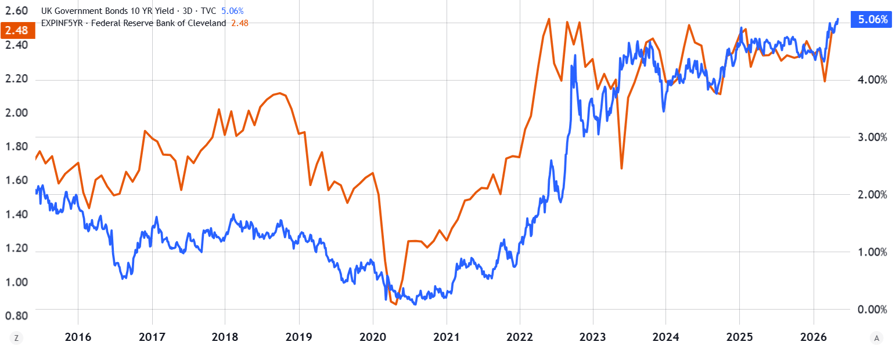

Expected inflation in the USA within 5 years and the yield of 10-year government bonds in euro. Source: TradingView

According to data from the Federal Reserve Bank of Cleveland, inflation expectations in the US have reached the highest level in 10 years, 2.5%. At the same time, investors are demanding higher yields from holding euro zone government bonds. Despite these inflationary pressures, the tech-heavy Nasdaq 100 index hit an all-time high on Tuesday, signaling a broader risk-on environment.

Declining Bitcoin onchain activity is associated with a gigantic accumulation of spot ETFs

Bitcoin may have benefited from increased risk appetite, but tender onchain metrics point to falling retail demand.

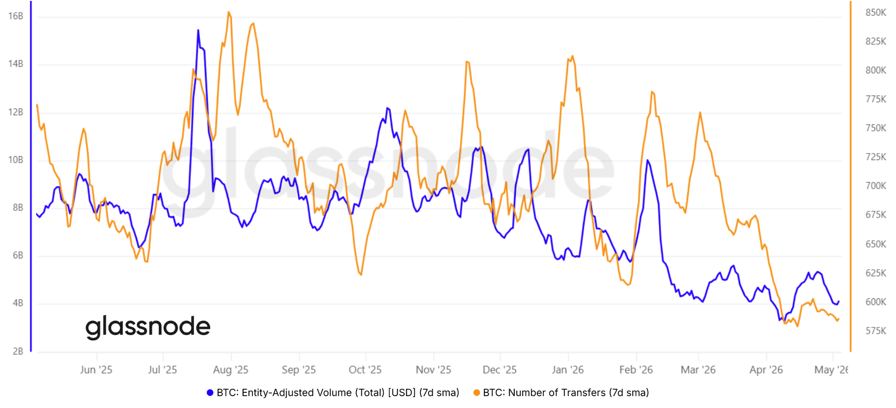

Daily volume of Bitcoin onchain (USD) and the number of transfers. Source: Glassnode/Cointelegraph

Daily network transfer volume dropped 54% from three months ago, to $4.1 billion. Similarly, the number of transfers is approaching its lowest level in over five years. While Bitcoin’s price action is not strictly dependent on on-chain activity, these metrics serve as a proxy for overall public interest and adoption.

The a fleeting break in the Strategy (MSTR US) accumulation prior to the publication of the results may have caused unjustified fear. The Michael Saylor-led company has maintained an aggressive acquisition pace over the past four weeks. However, analysts expect Strategy to report a quarterly net loss due to Bitcoin’s mark-to-market accounting.

Related: Bitcoin turns on risk as stocks hit novel highs and miners’ profits soar: Will 85k be next? BTC dollars?

Macroeconomic weakness and failing supply chain activity have negatively impacted Bitcoin derivatives, but… Net proceeds of $1.16 billion to US-listed spot Exchange Traded Funds (ETFs) Bitcoin in the period from Friday to Monday suggests growing institutional demand.

Ultimately, the lack of demand for leveraged bullish positions in Bitcoin derivatives could serve as a catalyst for further gains. As prices rise, those taking a compact position (sellers) may be forced to close their positions at a loss, further increasing momentum.

{kind=link}