Image source: Getty Images

Shareholders incl FTSE250 stocks had a terrible week. They haven’t really had much to be elated about over the past 18 months. From August 2024 to the present (March 9), the group’s share price has fallen by 67%.

But sometimes a discounted stock can be a bargain. Could that be the case here? Let’s talk.

What’s going on?

Vistra Group (LSE:VTY) was punished by investors last Wednesday (March 4). After the publication of its 2025 results, the company’s share price fell by 25.6%. The last time the construction company’s stock traded at this level was November 2012. Almost 14 years to nowhere is hugely disappointing.

Last week’s events are even more depressing considering shareholders probably thought the worst was over.

In October 2024, Vistry issued a profit warning after discovering that it had misreported some cost estimates. Embarrassingly, just four weeks later she had to announce that the situation was worse than the group had initially thought. The third warning was issued in December 2024 following a deterioration in trading conditions.

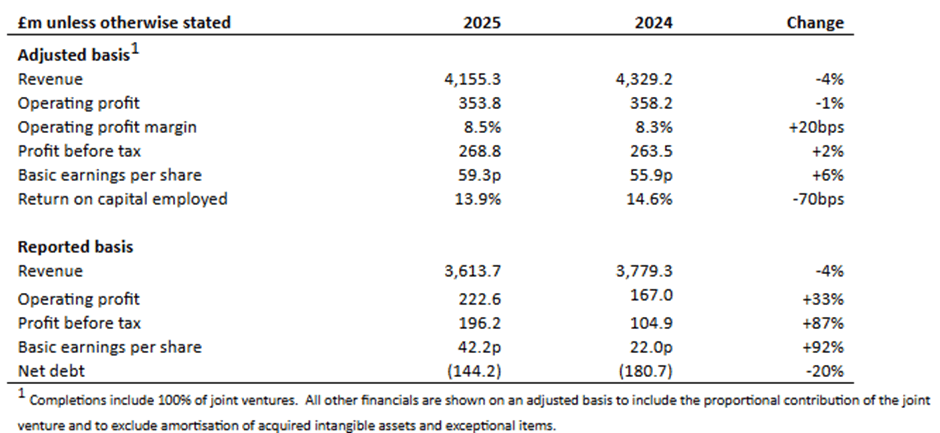

However, a closer look at the group’s 2025 results suggests investors may have overreacted last week. Adjusted earnings per share amounted to 59.3 pi and were 6% higher than in 2024. The company’s shares are currently trading at an attractive 7.8 times historical earnings.

However, the group warned that it was employing “targeted pricing and sales incentives“, which would lead to “lower overall marginStill, it expects to end 2026 with a net cash position.

I suspect that what upset the City the most was the decision to suspend the share buyback program. The group suspended dividend payments in 2023, using the saved money to purchase its own shares. This policy has now been scrapped as the group plans to employ excess cash to reduce its debt.

A different business model

What is unique about the group is that its primary focus is affordable housing, commonly defined as “apartments for sale or rent for people whose needs are not met by the market“. In 2025, it built one of seven properties of this type in the country. It should therefore benefit from the government’s £39 billion Social and Affordable Homes Program (SAHP), which is to run for 10 years until 2036. The plan assumes financing 300,000 novel homes.

Even if the group fails to secure funding, many of its clients – including registered suppliers and local authorities – are likely to succeed. 74% of projects in 2025 were implemented under these partnerships.

Despite its recent woes, I think Vistra is worth a closer look. It maintains a forceful balance sheet and an order book of £4.5 billion. And despite hard market conditions, he managed to boost the average sales price in 2025.

However, it may take some time for things to start to improve, so the stock will likely only appeal to patient investors. I am confident that the group will be able to raise SAHP cash – no one in this market sector can match Vistra’s size and scale. However, given the planning red tape and all the other red tape involved in government contracts, I suspect it will be several years before these properties are built.

But overall, I think this stock should be considered by long-term investors.

{kind=link}