Quantum computing has become the latest catch-all explanation for Bitcoin’s recent decline in value, but NYDIG says the numbers don’t support the narrative. In a February 17 research note, NYDIG head of research Greg Cipolaro argues that “quantum fears” are thunderous, but not the primary driver of sell-offs when looking at search behavior, inter-asset correlations and broader risk positioning.

Quantum panic did not sink Bitcoin

NECESSARY frames “Cryptographically Relevant Quantum Computers” as investors continue to circle around theoretical downstream risk. The problem is that the market behavior does not look like a change in the valuation of an immediate existential threat.

First, Cipolaro points to Google Trends. He wrote that search interest for “quantum computing bitcoin” has increased, but time is of the essence. “There has been an increase in search interest for ‘bitcoin computing’, but this has particularly occurred as bitcoin has surged to new all-time highs rather than sustained weakness,” the note reads.

“In other words, increased search volume on quantum risk coincided with price strength rather than weakness. If the market were to re-price bitcoin on an immediate technological threat, we would expect the search intensity to lead to or increase downside risk, rather than accompany a period of upside.”

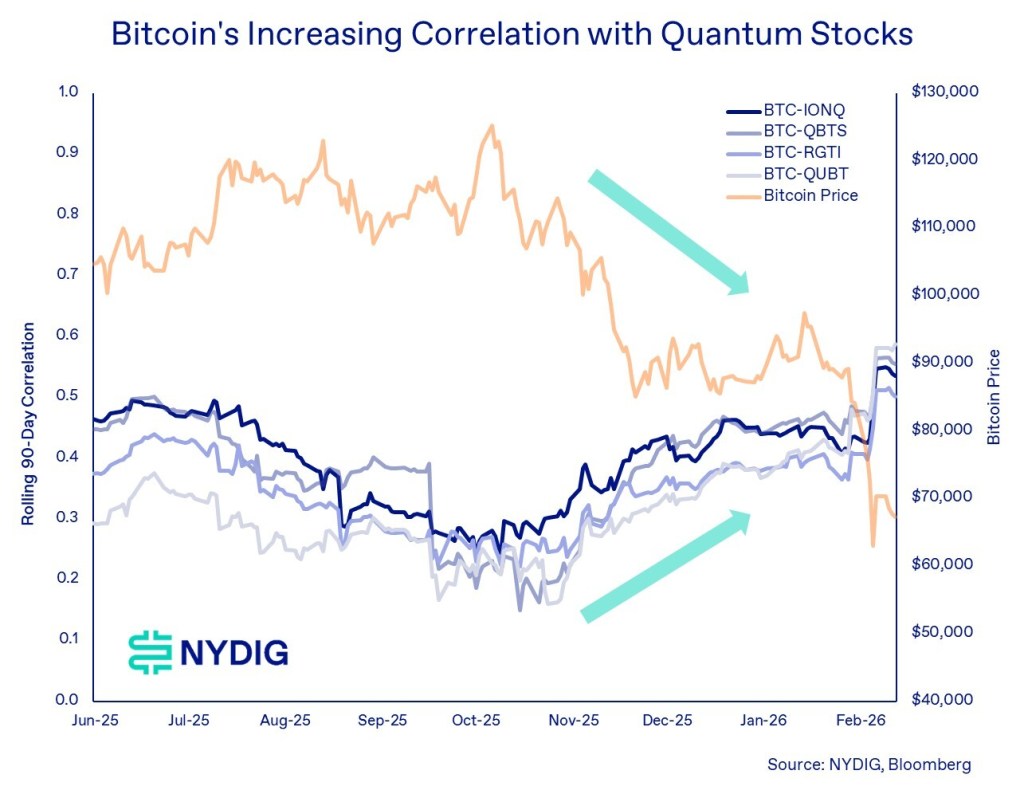

Second, NYDIG analyzes Bitcoin trading versus publicly traded quantum computing stocks, specifically IONQ, QBTS, RGTI, and QUBT. If investors were pulling out of Bitcoin as quantum progress was “catching up,” you would expect stocks related to the cryptocurrency to vary significantly as Bitcoin’s value declines. NYDIG claims the opposite was true. Bitcoin was positively correlated with these stocks, and these correlations strengthened during the drawdown, suggesting a common factor rather than direct quantum causality to Bitcoin.

NYDIG’s conclusion is clear on this matter. “The data does not provide evidence that quantum computing is the direct cause of Bitcoin’s weakness, even though that is currently the dominant risk narrative,” Cipolaro wrote. “A more likely explanation is a broader macro repricing of risk for long-term, expectation-based assets. Bitcoin’s recent drawdowns seem more consistent with changes in overall risk appetite than with any discrete technological catalyst.”

The mechanism that NYDIG draws attention to is familiar to anyone who observes liquidity regimes. He argues that quantum computing companies are long-term expectations-based assets with minimal revenues and high EV/revenue multiples. Bitcoin, while structurally different, is often a long-term bet on future adoption and monetary dynamics. When risk appetite declines, both may be hit together.

Meanwhile, NYDIG is flagging a divergence in derivatives markets that it believes reflects the current state of affairs better than quantum headlines. The one-month annual interest rate on the CME is “holding above” Deribit, which NYDIG uses as a proxy for U.S. onshore institutional positioning versus offshore positioning.

Structurally, the higher CME basis means that US markets have behaved more constructively, while the sharper decline in the 1-month Deribit basis indicates increasing caution in overseas markets and reduced appetite for leveraged long exposures.

At the time of publication, Bitcoin’s price was $66,886.

Featured image created with DALL.E, chart from TradingView.com

{kind=link}