Image source: Getty Images

Prices of analysts for Lloyds Banking Group (LSE: lloy) Actions are not particularly ambitious at the moment. But there are clear ways in what things can be better than expected.

Interest rates, ongoing legal (yes, really) and hearty dividend are positive signs of the bank. So is it possible to buy for investors?

Target

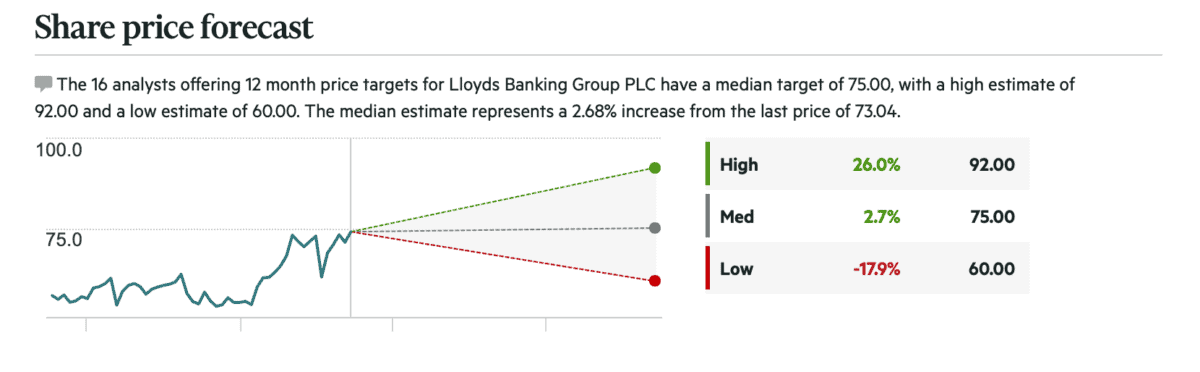

It can be safely said that analysts are quite divided into the prospects of Lloyds Banking Group. The target median price is 75 pence – about 3% higher than the level to which the actions currently trade.

However, there is a fairly immense range. The highest estimation is 26% higher than the current price of shares, and the lowest implicitly implies a 18% decrease.

Investors should, however, notice that the dividend performance is about 4.5%. If this is continued, this can provide a return with a 10-year government bond, even if the actions do not go anywhere.

The company also has an action purchase program that should facilitate augment the value of shares. And I think there are more reasons why the optimism is continued.

Interest rates

I always consider it a risk when the company’s profitability depends on something except for its control. And this is the case with Lloyds and what the Bank of England is doing with interest rates.

The central bank in Great Britain decided to reduce the rates at the beginning of this month and it probably will not be harmful to margins. But I think investors have several reasons for optimism.

One of them is that the Bank of England indicated that it is to be careful in future decisions. So it is far from automatic that interest rates will fall in the near future.

Another is that cuts have a greater impact when the rates are low – 1% to 0.75% is more significant than 3% to 2.75%. Therefore, a reduction from 4.5% to 4.25% may not be a huge problem.

Motor loans

Another main continuous problem is the legal matter regarding motor loans. Lenders, including – among others – Lloyds refer to the verdict of the Court of Appeal in October 2024.

A sentence is expected in the next few months. This can have a huge impact on the company’s price in one way or another.

Lloyds put away about 1.2 billion GBP to cover potential obligations. This is about 66% of what the company distributed in dividends in 2024.

Analysts estimate that the worst scenario of the bank may be obligations about four times at this level. But if everything goes well, the shareholders could be in a state of powerful return.

Shares to consider the purchase?

The average target price of analytics for Lloyds shares is similar to the current level. But there is a immense range, which now reflects a lot of uncertainty.

No company never has complete control over its profits. However, in the case of Lloyds, an extremely immense number of his future phrases boils down to things with which he can do nothing.

At the right price it is a risk, I think investors could rightly consider taking up. But I think that there are more attractive opportunities in British actions.

{kind=link}