Image source: Unilever plc

I really like the investment thing Unilever (LSE:ULVR). Other investors seem to feel the same way. Unilever’s share price is up 23% this year.

For a company with a long tradition, operating in a mature industry and selling everyday products, this seems like a huge leap.

Why I like the investment case

First, let me explain why I like the Unilever investment case overall.

It operates in an area where there will likely be high and sustained demand for decades (dare I say, perhaps even centuries) to come. Shampoo and laundry detergent may not be invigorating business areas, but I don’t think they’ll go away anytime soon.

Such markets tend to attract a horde of companies eager for a piece of the pie. Having spent decades investing in building premium brands such as Pigeon AND MarmiteUnilever helped it stand out from the crowd.

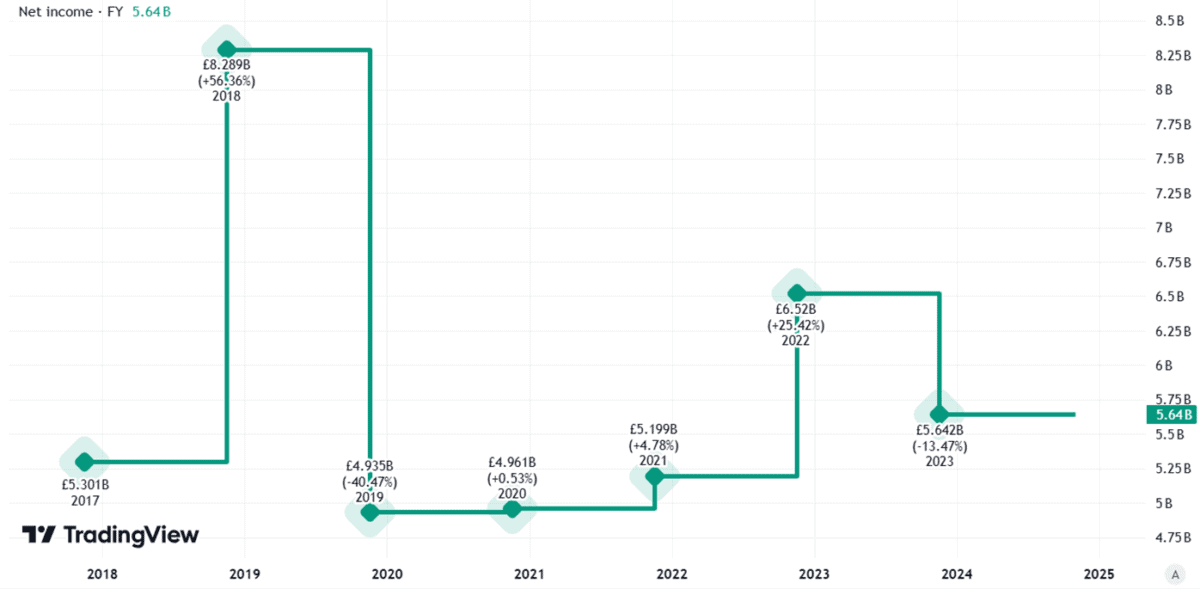

This gives it pricing power, which in turn helps generate profits. Yes, the company’s profits have fluctuated in recent years. But they kept running into billions of pounds.

Created using TradingView

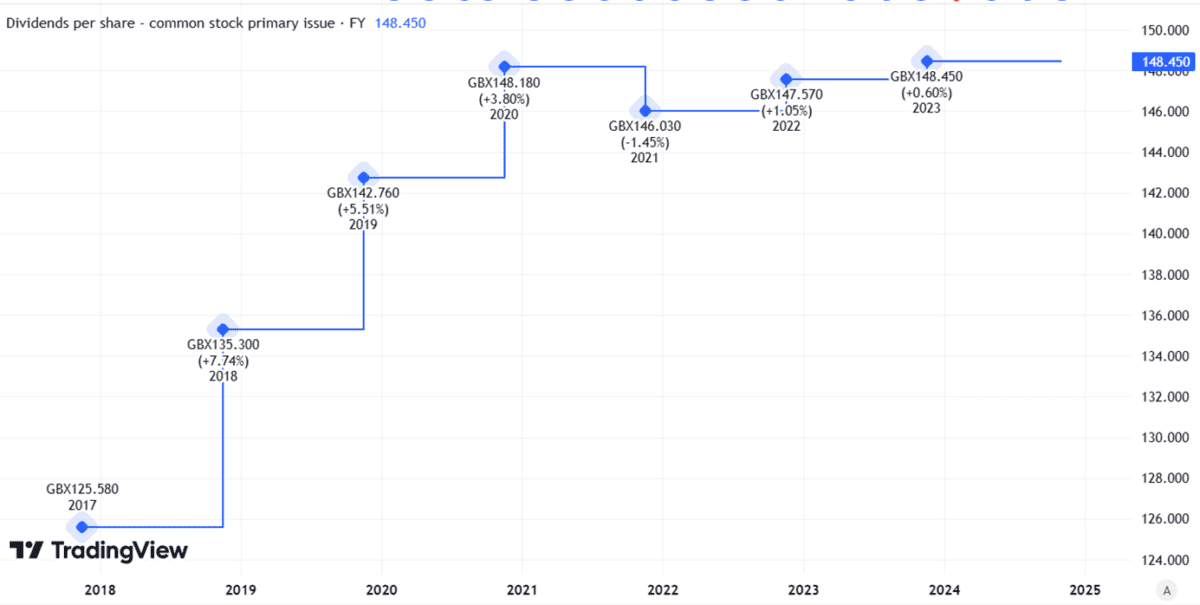

This, in turn, helps finance dividends.

Created using TradingView

Back to Warren Buffett’s attempt to take over

Is it a coincidence that in 2017 Warren Buffett tried to buy Unilever – not some of its shares, but the entire scandal?

I would say not at all.

Unilever has all the hallmarks of a classic Buffett investment: a huge, sustainable market, forceful competitive advantages and proven cash-generating potential.

Understanding recent price movements

Buffett failed. It was £40 a share. However, since then, Unilever’s share price has repeatedly fluctuated below (in fact, well below) this price.

So why has it increased this year?

New management may be part of the explanation. Plans to cut jobs at a huge multinational corporation herald the prospect of lower costs, potentially increasing profit margins.

A plan to spin off the ice cream industry and focus on areas such as personal beauty could look similar, with attractive margins and no need for a convoluted icy chain supply chain. Croissant factory to corner store.

Last week’s investor event confirmed it was on track to meet its cost-cutting goals, and the company also outlined its “Roadmap for growth to 2030“. The company said it is on track to separate its ice cream business from the rest of the company by the end of next year.

I don’t like the stock price

Still, it seems like pretty tardy progress to me. This suggests that for the right price, buyers might not have chewed a bite (or at all). Ben and Jerry).

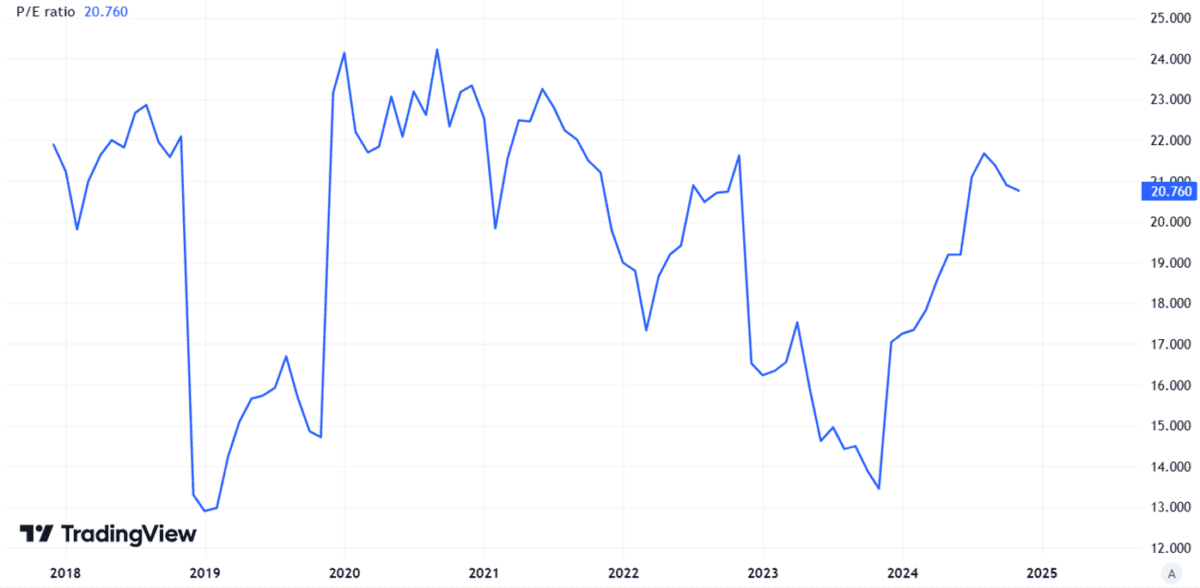

Meanwhile, development plans are fine (although they may be arduous to implement in such a mature business), but they are based on them current results, the ratio of Unilever’s share price to profits is already 21.

Created using TradingView

I don’t think it’s outrageous, but it’s higher than I feel comfortable with as a potential investor, even though I like the Unilever investment case.

The company faces risks ranging from selling to the ice cream business at a price too low to get rid of, to a faint economy that’s causing demand for branded products to decline. So for now I have no plans to add Unilever to my portfolio.

{kind=link}